Rastra Bank last sent money to the market through repo on 23 Chait 2079. Since then, funds have been withdrawn from the market every week as required. According to the Rastra Bank, 319 trillion 84 billion 15 billion rupees were withdrawn from the market 1,075 times.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

Rastra Bank has been continuously withdrawing money from the market for two and a half years. After accumulating loanable funds (excess liquidity) in the financial system, the National Bank is drawing money through various monetary instruments for management.

Rastra Bank last sent money to the market through repo on 23 Chait 2079. Since then, funds have been withdrawn from the market every week as required. According to the Rastra Bank, 319 trillion 84 billion 15 billion rupees were withdrawn from the market 1,075 times. Out of that, about 6 trillion 80 billion rupees remain (outstanding) despite returning to the market after the maturity period.

Rashtra Bank Spokesperson Kiran Pandit said that due to the problems seen in the economy, due to the lack of credit demand, there is a situation of excess liquidity in the financial system. There was a slowdown in the economy due to various reasons. This resulted in a decrease in effective demand, due to which the demand for credit also decreased. However, remittances were coming in well. Imports also did not increase as expected. Due to the lack of credit demand, the situation of excess liquidity remained a

,' he said, 'As it is the job of the National Bank to maintain stability in interest rates, the interest rate corridor is being operated for that purpose. Under the same process, liquidity has been extracted from the market from time to time as needed.'

Although loans are seen in auto, shares and other sectors, there is no demand for loans in other sectors, so there has been more liquidity for a long time. - Ashok Sherchan, Chief Executive Officer, Prabhu Bank Experts say that the economy is in a state of 'liquidity trap' due to long-term high liquidity, low interest rates, and the lack of conditions to further reduce interest rates to make the economy viable. Interest rates have fallen to their lowest level in 49 months. Banks and financial institutions have 10 trillion 18 billion rupees of excess liquidity as of last Monday.

In two and a half years, the National Bank withdrew 319 trillion 84 billion 15 billion rupees from the market 1075 times, after the maturity period, the amount was returned to the market, but about 6 trillion 80 billion rupees remained According to Parshuram Kunwar Chhetri, a former banker and an expert in the banking sector, more liquidity has been added to the financial system due to the failure to expand loans in proportion to the increase in deposits. Compared to June, until last Monday, deposits decreased by 61 billion and loans decreased by 26 billion. It is natural for deposits and loans to decrease in the first month of the financial year," he said. "Looking at the situation of more liquidity, it seems that this situation will remain the same for a few more months."

Due to the exodus of a large number of young people, the market demand has decreased, says Kunwar. In the last four years, about 3 million Nepalis have gone abroad for employment and about 500,000 youths have gone abroad for study. Many Nepalis have gone abroad through informal means as well. Even if we consider only about 500,000 people who went that way, about 400,000 youths left in four years," he says.

Business does not grow until demand increases. When the business does not expand, the demand for bank loans does not increase. To increase the market demand, Kunwar suggests that the government should increase the expenditure to make the economy viable.

According to the directives of the National Bank, banks and financial institutions can provide loans up to 90 percent of deposits. Banks must keep a minimum of 20 percent of deposits in cash for potential savings returns. By reducing the amount of cash required, banks and financial institutions can maintain a CD ratio of up to 89 percent.

The direct impact of the youth leaving has hit the market, the business will not grow until the demand increases, if the business does not expand, the loan demand will not increase. - Parashuram Kunwar, Chhetri ex-banker The same amount is analyzed here as the loanable amount. In this way, as of last Monday, the amount that can be loaned is 9 trillion 44 billion rupees.

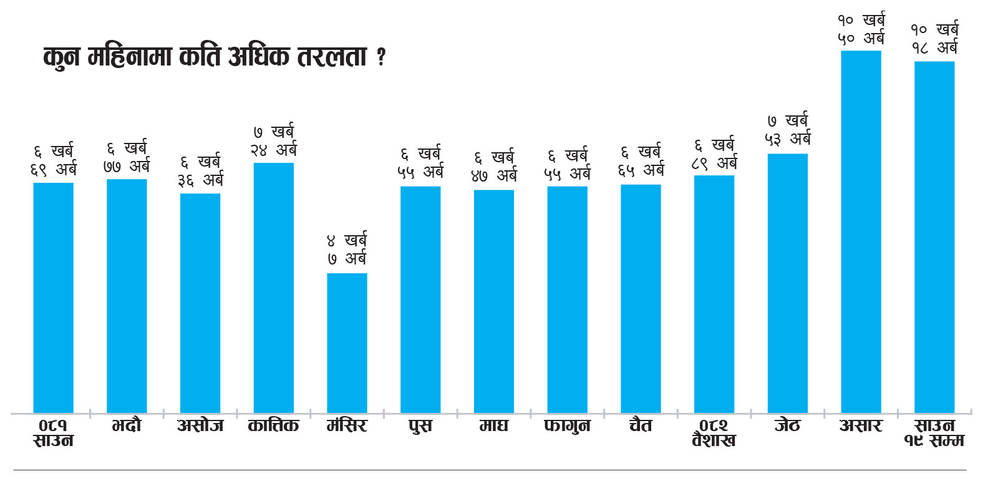

Banks and financial institutions had excess liquidity of 6 trillion 69 billion rupees in July last year. 6 trillion 77 billion in August, 6 trillion 36 billion in October, 7 trillion 24 billion in October, 4 trillion 7 billion in November, 6 trillion 55 billion in January, 6 trillion 47 billion in January, 6 trillion 55 billion in February, 6 trillion 65 billion in March, 6 trillion 89 billion in Baisakh, 7 trillion 53 billion in May and 10 trillion 50 billion in June.

Since the beginning of the financial year is in July, usually both deposits and loans decrease. As the interest on the deposit comes in the middle of June, the depositor withdraws it to fulfill the requirement. At the end of the financial year, the bank will try to recover as much as possible and the debtor will also try to pay the principal and interest, so new loans will not be issued and the old ones will also decrease.

Rastra Bank had set a target to expand loans by 12.5 percent in the last financial year. To fulfill this, banks and financial institutions had to extend loans of 6 trillion 82 billion rupees. But until last May, the loan disbursed by the banks was 2 trillion 85 billion rupees less than the target. For the current financial year, the National Bank has set a target of about 12 percent credit expansion.

Prabhu Bank Chief Executive Officer Ashok Sherchan said that banks and financial institutions could not extend loans as expected due to the lack of demand for loans in the market. No new loans have been issued. Auto, shares, real estate have seen loans in some areas, but other loans have been recovered in the same amount. Overall, credit has not been able to expand," he said, "due to which there has been excess liquidity in the financial system for a long time. To manage it, the National Bank is constantly drawing money from the market.'

It is seen that the loanable capital (more liquidity) in banks and financial institutions will increase even more. Sources say that due to continuous increase in remittance flow, money for government expenditure starting to come to the market, and restrictions on consumption, even though deposits are increasing, there is no expected improvement in credit flow, the amount that can be loaned to banks and financial institutions will increase.

Rastra Bank has been withdrawing money from the market for two consecutive days (Sunday and Wednesday) for one and a half years because the loan amount is too much. In the previous year, withdrawals were made for short periods (7, 14, 21 days). Recently, the National Bank has been withdrawing money for 35 days, 42 days, 63 days. An official of Rashtra Bank has informed that money has been drawn for a few more periods recently in anticipation of increasing liquidity in the financial system. The report also showed that the National Bank had to spend a large amount of money for liquidity management.

How to withdraw money from the market?

Monetary policy also aims at financial stability and interest rate stability. For this the liquidity (money in the market) should remain within the desired limits. The National Bank has been conducting open market transactions. It means sending and withdrawing money in the market as per the need according to various monetary instruments. The National Bank uses short-term and long-term instruments to send and withdraw money from the market.

To ensure that the interest rate does not fluctuate abnormally but remains within the desired limit, the National Bank has launched the 'Interest Rate Corridor'. Under the corridor, three limits of interest rates are fixed, upper, middle and lower. At present, the upper limit (ceiling rate) has been maintained at 6 percent. This rate is the interest rate paid by banks and financial institutions when they take loans from the National Bank. The middle rate (policy rate) is 4.5 percent. It is the overnight repo rate at which banks borrow for one day. The lower limit (floor rate) has been fixed at 2.75 percent. This is the interest rate that banks and financial institutions get when the National Bank withdraws money from the market through deposit collection.

The upper and lower limit rates of the corridor have been adjusted by the Rastra Bank with inter-bank interest rates. Therefore, the National Bank tries to keep the interbank rate around the policy rate as much as possible. Even if this is not possible, it tries to keep within the lower and upper limits of the corridor. At the same time, when the interbank rate falls to the lower limit, the National Bank withdraws money from the market through various instruments. When the interbank interest rate approaches the upper limit, the central bank sends money to the market through various instruments. Since the interbank interest rate has been below the lower limit of the corridor for 2 and a half years, the National Bank is drawing money through various instruments.

'Economy is in liquidity trap, state should increase investment'

Nar Bahadur Thapa economist and ex-executive director of Rashtra Bank

Nar Bahadur Thapa economist and ex-executive director of Rashtra Bank

There has been more liquidity in the financial system for about two and a half years. The National Bank is constantly drawing money to manage it. How do you analyze this situation?

Over two and a half years of excess liquidity in the market means that the economy has entered a 'liquidity trap'. This means that there is more liquidity in the economy, the interest rate is very low and in such a situation, there is no possibility to reduce the interest rate or it is not possible to accelerate the economy by reducing the interest rate.

Monetary policy does not work after a country is in a severe liquidity trap. In order to make the economy sustainable, the system has been relaxed including increasing the limit of real estate purchase, reducing the risk burden of share loans, increasing the limit of individual share loans, working capital loan guidance and blacklisting. But the current problem will not be solved by these arrangements. These arrangements may provide relief to certain borrowers but will not improve the economy as a whole. These are just arrangements brought in to cover up that we will improve the economy.

The state is not doing what it should do but blaming other agencies including Rashtra Bank, working capital loan guidelines etc. But why the credit in the market did not expand? Why is money accumulating for a long time? It has not been effectively discussed.

What are the ways to overcome this situation of the overall economy and financial system?

Overall demand has not increased due to lack of money in the hands of citizens. The cycle of cash flow of citizens (consumers) has also been broken due to the problems seen in cooperatives, microfinance and other sectors. Due to the problems in these areas, banks and financial institutions have also been affected on the one hand, and on the other hand, many young people are forced to go abroad. This has reduced the overall demand. This situation should be improved.

In order to increase the market demand, the consumption tendency of citizens should increase. At present, private investment has not increased. Therefore, the only way to solve the problems of the economy is to increase government spending. Investments are of two types – one, motivated by profit

s are induced and others are not profit-driven (autonomous). Private sector investment in particular is profit driven. As there is no possibility of profit in the current situation, it is not likely to increase. Therefore, the government should increase the 'autonomous' investment to a large extent. It is the government to save the system, the state, the country. Domestic and foreign investors are attracted only when the government accelerates the economy by increasing investment.

Then, in which areas should the government increase investment?

First of all, the government has to pay the arrears due to the obligation. For example, the government should immediately pay the dues of sugarcane farmers, health insurance, corona insurance, interest subsidy, agricultural insurance premium, export subsidy, construction business etc. Due to the payment of dues, the money goes to the market, so it reaches the hands of the citizens and the economic activity runs. After that, the government should increase investment in projects that give quick returns.

Since the beginning of the current financial year, there is more than 10 trillion excess liquidity in the financial system. As July is coming to an end, the demand for credit does not seem likely to increase. Can this situation be understood as a sign that the banks are only hoarding money this year?

loan demand has not increased. It is also said that many borrowers do not pay interest at all. Some say they have paid interest and debt. It is heard that many of them have taken loans from banks and paid the principal and interest. Such credit expansion does not contribute to economic growth, nor does it contribute to national capital formation. There is no possibility of improvement in the present situation unless there is demand for credit from the real sector.

What can the National Bank do to improve this problem?

National Bank cannot do anything. The government will take the lead in solving the current problem. National Bank and other agencies will only assist or facilitate the work of the government.