The personal income tax reform proposal launched this year should be effectively implemented and the process of further reform should be initiated. In that context, the 'mini income tax' implemented in the name of 'social security tax' should be reviewed.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

Subject Introduction

The personal income tax reform is one of the various tax reforms implemented by the budget for the fiscal year 2083/84. It has three main features.

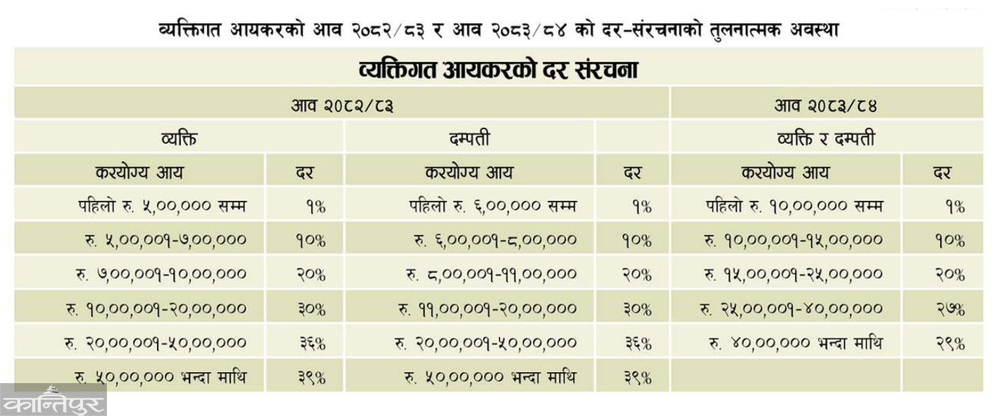

First, it has implemented a single unified tax schedule instead of maintaining separate tax schedules for individuals and couples. Second, it has increased the exemption of Rs. 5 lakh for individuals and Rs. 6 lakh for couples to Rs. 1 million for all taxpayers. Third, it has abolished the tax rates of 30, 36 and 39 percent and has established marginal tax rates of 27 and 29 percent for high income earners.

The comparative status of the rate structure of personal income tax for the fiscal year 2082/83 and fiscal year 2083/84 is given in the table below:

Progressive structure

According to the principle of personal income tax and international common practice, the rate structure of personal income tax in Nepal is progressive, under which the marginal tax rate also increases as the taxable income increases. Until the fiscal year 2082/83, the upper marginal rate was 39 percent, which was the highest in South Asia.

Such a high rate was not suitable for making our economy competitive, attracting work, savings and investment, expanding the formal sector, encouraging voluntary tax compliance and discouraging tax evasion. Therefore, various organizations and experts have been suggesting that the number and level of tax rates should be reduced to make Nepal's personal income tax system similar to the systems of other Asian and comparable countries.

The personal income tax reform proposal launched this year should be effectively implemented and the process of further reform should be initiated. In that context, the ‘mini income tax’ implemented under the name of ‘social security tax’ should be reviewed. For example, the 'High-Level Tax System Review Commission' formed by the Government of Nepal in 2071 BS under my chairmanship had proposed three rates of 10, 20 and 30 percent for personal income tax. The 'High-Level Tax Reform Suggestion Commission' formed by the Government in 2081 BS under the chairmanship of Bidhyadhar Mallik had also suggested three rates of 10, 20 and 25 percent for personal income tax and a 20 percent charge on the final slab of tax for taxpayers with an annual income of more than Rs. 5 million.

Finally, the budget for the fiscal year 2083/84 has improved the personal income tax rate structure by fixing the highest marginal rate at 29 percent and also reduced the number of rates. This has simplified the tax rate structure, made the tax system more competitive, and made the tax more neutral or efficient from an economic perspective. And, it is expected to encourage tax compliance.

Although the reduction in the highest marginal rate of tax has somewhat reduced the overall progressivity of the tax system, the revised structure has internalized the progressivity of personal income tax as the marginal tax rate increases with income.

The new structure of personal income tax rates is expected to increase horizontal equity. Remember, in the past, a large portion of personal income tax was collected from employees in the formal sector, including public, private, and cooperatives, who were taxed at source. Since the tax rate was very high, the self-employed, high-income earners, and informal sector earners tended to stay out of the tax net as much as possible. This meant that the burden of personal income tax on income from different sectors was not evenly distributed, leading to horizontal tax inequities. The reduction in the marginal tax rate would encourage the self-employed and informal sector earners to come under the tax net. In addition, a campaign should be launched to effectively tax all types of income earners equally by strengthening taxpayer registration, third-party information reporting, data reconciliation, tax audits, and tax law enforcement.

Unified tax schedule for individuals and couples

The proposed reform replaces the current separate tax schedules based on marital status with a single tax schedule for both individuals and couples. This change will strengthen horizontal tax justice by ensuring that taxpayers with the same taxable income, regardless of whether they are single or married, generally have the same tax rate.

The Unified Tax Schedule will reduce the impact of marital status on tax liability and simplify the tax system. In particular, it is expected to make tax deduction at source, income tax return filing and tax administration simpler, clearer and more uniform.

Inflationary tax bracket increase

In the past, when the taxable income brackets (slabs) were narrow and the first income bracket of tax exemptions remained unchanged for a long time, taxpayers were in a situation where they entered a higher tax bracket even though their real purchasing power did not increase due to inflation or monetary wage growth. This is called inflationary tax bracket increase (bracket creep). The significant increase in the first income bracket of tax exemption in the fiscal year 2083/84 and the subsequent widening of taxable income brackets have corrected the impact of inflationary tax bracket increase accumulated in previous years to some extent.

This reform is only a one-time adjustment. This effect may gradually re-emerge if there is no mechanism to periodically adjust the tax brackets to inflation or wage growth. To address this problem in the long term, a transparent mechanism to review the tax brackets at regular intervals should be established.

Administrative simplicity

The proposed system will be easy to understand and administer, with a single tax schedule for individuals and couples and a reduced number of tax rates. The reform is expected to simplify tax withholding at source, the process of filing income tax returns, communication with taxpayers, and monitoring tax compliance, as well as reduce disputes over marital classification.

Revenue and economic impact

The system of tax deduction at dozens of sources is administratively complex and economically inefficient, and it should be simplified. The increase in the first income bracket, the expansion of other income brackets, and the reduction in the marginal tax rate are expected to reduce personal income tax revenue collection in the short term. However, the reform is expected to increase revenue collection as it will increase voluntary tax compliance, reduce tax evasion, expand the formal sector of the economy, support investment and economic activity, and increase employment.

In addition, since the reduction in personal income tax liability will increase the disposable income of the taxpayer, it can be expected that household consumption will increase, which will indirectly increase the collection of value-added tax, excise duty and customs duty revenue.

Tax compliance concessions

The budget for the fiscal year 2083/84 has announced a special relief program to encourage voluntary tax compliance and resolve outstanding tax liabilities.

According to the proposed arrangement, taxpayers who have not collected, filed, submitted or paid taxes in the past will be able to get exemption from interest, fines, additional fees and late fees if they fulfill certain conditions. To get such concessions, the taxpayer will have to submit the outstanding details and pay the principal tax amount and an additional amount equal to 1 percent of it within the stipulated time.

This relief arrangement has been made applicable to cases pending under the tax assessment, revised tax assessment, administrative review, judicial appeal and revenue leakage laws.

These measures are expected to facilitate dispute resolution, increase revenue collection and encourage taxpayers to regularize their tax liabilities and resolve the problem that has been pending in tax implementation for years. The terms and time limits of this program should be widely publicized and implemented transparently.

Since repeated tax amnesty programs may delay tax compliance by taxpayers in the hope of getting concessions in the future, such programs should be limited to a certain period. And, after the program ends, the implementation of tax laws should be further strengthened.

Other reforms

Similarly, the budget for the fiscal year 2083/84 has recognized capital gains tax received from the sale of securities of listed companies as a final tax. This has addressed the long-standing demand of investors and stakeholders in the capital market.

Similarly, a resident natural person has been provided with a provision to pay personal income tax on the remaining amount by deducting 25 percent of the annual amount paid for the education of his/her children or Rs. 25,000, whichever is less, from the taxable income.

The personal income tax reform proposals launched this year should be effectively implemented and the process of further reform should be initiated. In that context, the 'mini income tax' implemented in the name of social security tax should be reviewed. Since the system of tax deduction at dozens of rates is administratively complex and economically inefficient, it should be simplified. Efforts should be made to maintain horizontal equality by expanding the tax scope in administrative terms and implementing taxes uniformly in all sectors.

The feasibility of implementing an indexation system should be studied to solve the problem of inflationary tax rate increase. Initial preparations should be started to implement pre-filled tax returns. And, our personal income tax system should be established as the best tax system in the world within two to three years by making similar reforms.