Slow economic activity, failing market demand, industries operating at only 42 percent capacity, and a stock market that has failed to rise have not led to an increase in credit flow.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

With only one week left for the end of the current fiscal year (as of 25 Ashar), banks and financial institutions have accumulated a loanable amount (excess liquidity) of Rs 1.56 trillion. As deposits have increased due to low loan demand and increasing remittances, the amount of loanable capital in banks and financial institutions has been increasing continuously in all months of the current year.

Experts say that loanable capital has accumulated in banks and financial institutions due to factors such as the failure to increase market demand, sluggish economic activity, industries operating at only 42 percent capacity utilization, and the stock market failing to rise. Although liquidity has been high in the last three years, the amount of liquidity is high this year.

According to the data of the National Bank, as of 25 Ashar, around Rs 1.56 trillion has accumulated in banks and financial institutions. The total deposits of banks and financial institutions during the same period are 8.267 trillion. The loan-deposit ratio (CD ratio) during the same period is 71.29 percent.

According to the instructions of the National Bank, banks and financial institutions are allowed to lend up to a maximum of 90 percent of total deposits. During this period, the total credit flow of banks and financial institutions is 5945 billion. Based on the aforementioned data, the amount that can be given to banks and financial institutions as of mid-Ashar is 1560 billion 260 million rupees. However, banks and financial institutions must keep 20 percent of their total deposits in cash in the bank.

The amount that all banks and financial institutions must keep with them to maintain 20 percent liquidity is about 1 percent of the CD ratio. Based on this, although banks are allowed to lend up to 90 percent of deposits, in practice they are allowed to lend only up to 89 percent. Even when measured in this way, there is excess liquidity of 1476 billion 870 million rupees in banks and financial institutions as of 25 Ashar. Santosh Koirala, President of the Nepal Bankers Association, said that since the economy could not become dynamic and there was no demand for credit, banks were unable to lend as much as they wanted, and money was piling up.

‘Industries are operating at less than half their capacity utilization, new businesses have not opened. As a result, the demand for credit in the economy has not increased, so the credit flow has been less than expected,’ he said. ‘Economic activity should increase for credit to increase, government spending should increase for economic activity to increase, only then will the credit flow of banks increase.’ He said that even though banks are prepared for credit flow, they have not been able to do so due to low demand.

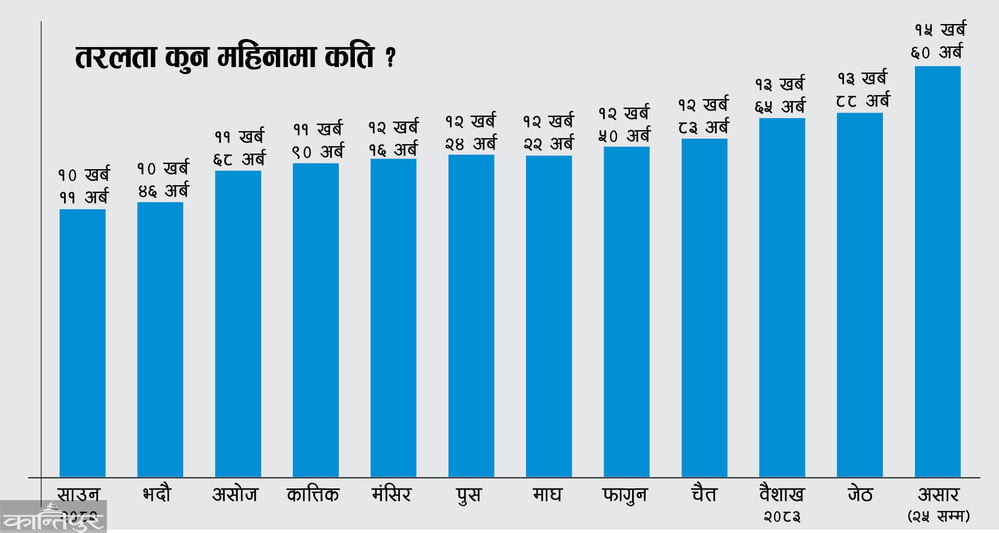

In the month of Shrawan of the current fiscal year, banks and financial institutions had excess liquidity of about Rs 100.11 billion. In Bhadra, Rs 100.46 billion, in Asoj, Rs 110.68 billion, in Kartik, Rs 100.90 billion, in Mangsir, Rs 120.16 billion, in Poush, Rs 120.22 billion, in Magh, Rs 120.50 billion, in Chaitra, Rs 120.83 billion, in Baisakh, Rs 130.65 billion and in Jestha, according to the data of the Nepal Rastra Bank.

Despite sufficient liquidity, more than half a dozen banks are unable to lend more due to capital pressure. With the primary capital (Tier One) of these banks remaining at the minimum limit, even if they have money, those banks are not in a position to lend much. Therefore, experts say that all the excess liquidity in the entire financial system is not in a position to lend.

Officials of the Nepal Rastra Bank admit that excess liquidity is increasing in the financial system due to the failure to expand credit as expected. 'External indicators are getting stronger and remittance inflows are increasing, which has led to an increase in deposits in the market. This has increased liquidity. There is an additional challenge in liquidity management,' said Satyendra Timilsina, Head of the Research Department of the Nepal Rastra Bank. He said that liquidity will be gradually utilized after the implementation of the policy arrangements in the monetary policy.

The fact that the Nepal Rastra Bank is continuously withdrawing money from the market confirms that liquidity management is becoming challenging. The Nepal Rastra Bank is withdrawing money from the market at least twice a week. As liquidity did not seem to be decreasing immediately, the National Bank had withdrawn Rs 200 billion for one year by issuing bonds last December. Its maturity period has not yet expired.

Last week, the National Bank has again withdrawn Rs 200 billion from the market for one year by issuing the same bond. The National Bank, which had withdrawn Rs 200 billion through bonds until Tuesday, withdrew Rs 100 billion from the market for 91 days through the deposit collection tool on Wednesday. This also confirms that liquidity management is becoming complicated.

Financial sector expert and former banker Parashuram Kunwar said that the expected flow of credit has not been achieved due to lack of market demand. ‘It is not that businessmen take loans and keep them at home. They start new businesses with loans or expand old ones. For this, market demand is needed. When demand does not increase now, businessmen have not been able to increase their business,’ he said, ‘Since businessmen did not increase their business, loan demand did not increase. When loan demand did not increase, money was piled up in banks.’

Kunwar says that even after three and a half months of the formation of the new government, there is no enthusiasm among industrialists and businessmen. "If we start work by signing contracts in a hurry from the first week of Shrawan, there is a possibility that the demand for loans in banks will increase as government expenditure will increase," he said.

In the current fiscal year (from Shrawan to Ashad 25), while deposits of Rs 963 billion were collected, only Rs 354 billion were disbursed. In the same period last year, deposits were Rs 741 billion and loans were Rs 422 billion.

The National Bank has set a target of 12 percent credit expansion in the current fiscal year. Looking at the situation up to 11 months, Nepal Bankers Association President Koirala said that it is unlikely that the annual target will be met. It is said that credit will be expanded by 11 percent in the coming fiscal year. Accordingly, an additional Rs 6.5 trillion should be disbursed. Experts say that this target will also be difficult to achieve if the economic situation does not improve.

In the 11 months of the current fiscal year, among the loans invested by banks and financial institutions, the construction sector expanded by 15.1 percent, the consumer sector by 13 percent, the transport, communication and public services sector by 12.5 percent, the industrial production sector by 6.8 percent, the service industry sector by 4 percent, and the finance, insurance and real estate sector by 0.6 percent. However, during that period, the loan flow to the agriculture sector decreased by 2.4 percent.

Among the loans flowed from banks and financial institutions during the review period, trust receipt (import) loans increased by 36.7 percent, margin loans by 15.8 percent, hire purchase loans by 10.3 percent, real estate loans (including personal residential home loans) by 6.3 percent, demand and other working capital loans by 5.8 percent, and term loans by 4.3 percent. However, during that period, ‘cash credit’ loans decreased by 0.3 percent and overdraft loans by 0.4 percent, according to the data of the Nepal Rastra Bank.

As of mid-June 2083, 14.7 percent of the loans invested by banks and financial institutions were secured by current assets (agricultural and non-agricultural goods) and 63.6 percent by real estate collateral. In mid-June 2082, the share of loans secured by such collateral was 14.5 and 65.0 percent, respectively. In the last 11 months, the share of loans secured by commercial banks, development banks and finance companies increased by 6.3 percent, 5.6 percent and 3.9 percent, respectively, according to the report of the National Bank.