The economic bill, which the government uploaded to the Finance Ministry's website on 15th Jestha, was removed the next day, on the 16th. It was re-uploaded 2/4 hours later, with some changes and additions to tax rates and provisions.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

MPs have raised questions about Finance Minister Swarnim Wagle's repeated changes to tax rates through the economic bill in the days after he unveiled the budget for the upcoming fiscal year on 15th Jestha. MPs from the opposition party have even demanded a parliamentary investigation into Finance Minister Wagle, saying that he has repeatedly amended the economic bill.

The economic bill uploaded by the government on 15th Jestha on the Finance Ministry's website was removed the next day on 16th. It was re-uploaded 2/4 hours later, with some changes and additions to tax rates and provisions. Why did this situation come about? Where did Finance Minister Wagle amend which rates? Based on which acts and regulations were the rates revised?

The economic bill currently on the Finance Ministry's website is the third amendment. With each change, some tax rates have been reduced and some have been increased. Some have been given relief while others have been taxed heavily. MPs have also viewed this arbitrary change in tax rates since the day the budget was made public as a matter of concern and suspicion.

Where and what changes were made to the bill?

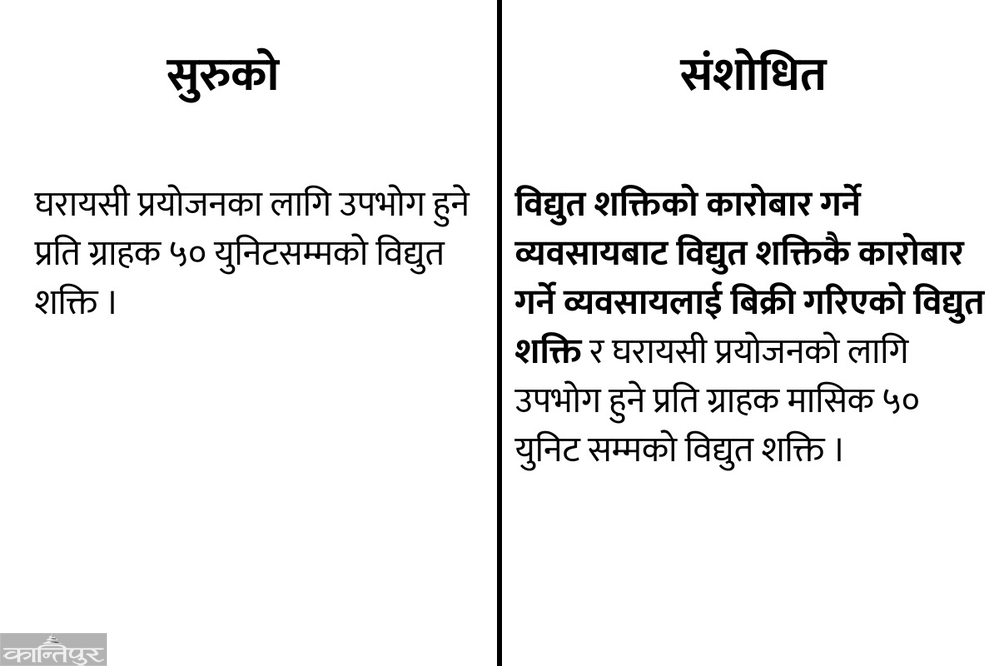

The main differences between the economic bill that was first uploaded on the website of the Ministry of Finance on 15 Jestha and the one currently there are as follows. First, the government had amended the Value Added Tax (VAT) Act to initially exempt electricity up to 50 units per consumer consumed for household purposes from VAT. This provision was mentioned in the VAT Act. In which, VAT was not levied on ‘electricity up to 50 units per consumer consumed for household purposes’, but it was levied on anything in excess of that. According to this provision, VAT was levied on sales from businesses trading electricity to businesses trading electricity (for example, when an electricity promoter sells to the Nepal Electricity Authority).

Now, the provision has been amended to exempt electricity traders and up to 50 units for household purposes from VAT. ‘Electricity sold by businesses trading electricity to businesses trading electricity and electricity up to 50 units per consumer consumed for household purposes per month’ is stated in the latest amended economic bill. The latest amendment has changed the business of electricity trading from a business that only trades electricity to a business that only trades electricity, but VAT will be levied on electricity consumed by more than 50 units per customer per month.

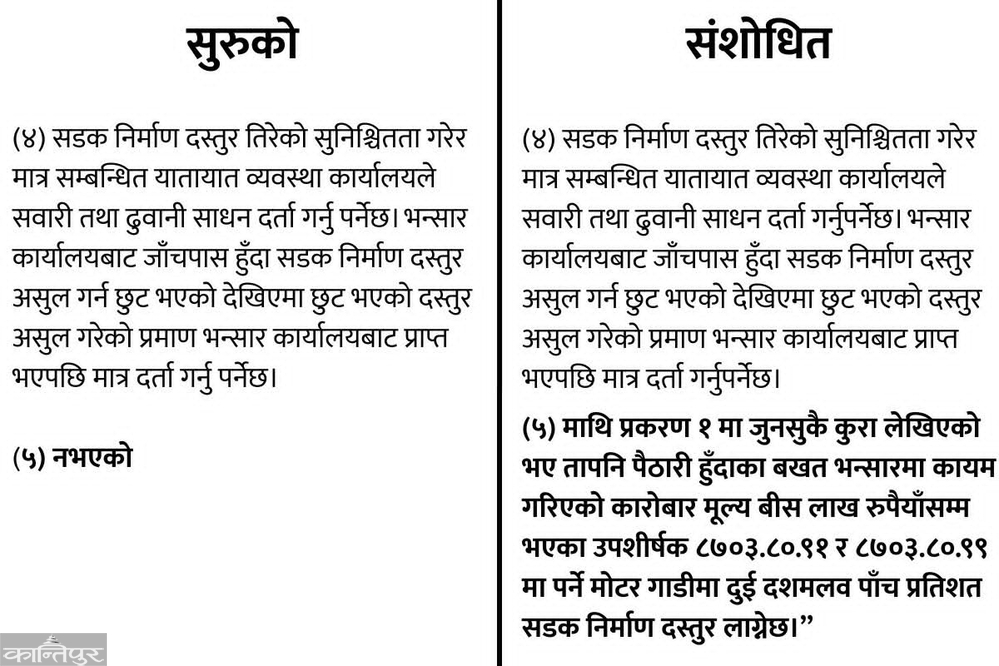

Second, as per the provisions of the latest bill, the government has reduced the road construction fee for electric vehicles worth less than 2 million rupees to 2.5 percent. Generally, the road construction fee was levied on all types of vehicles at 5 percent. The same provision was continued in the first bill made public on 15 Jestha. However, the provision has been revised in the latest bill. ‘Notwithstanding anything written in Chapter 1, a 2.5 percent road construction fee will be levied on motor vehicles falling under subheadings 8703.80.91 and 8703.80.99 with a transaction value of up to 2 million rupees determined at customs at the time of import,’ the latest economic bill states.

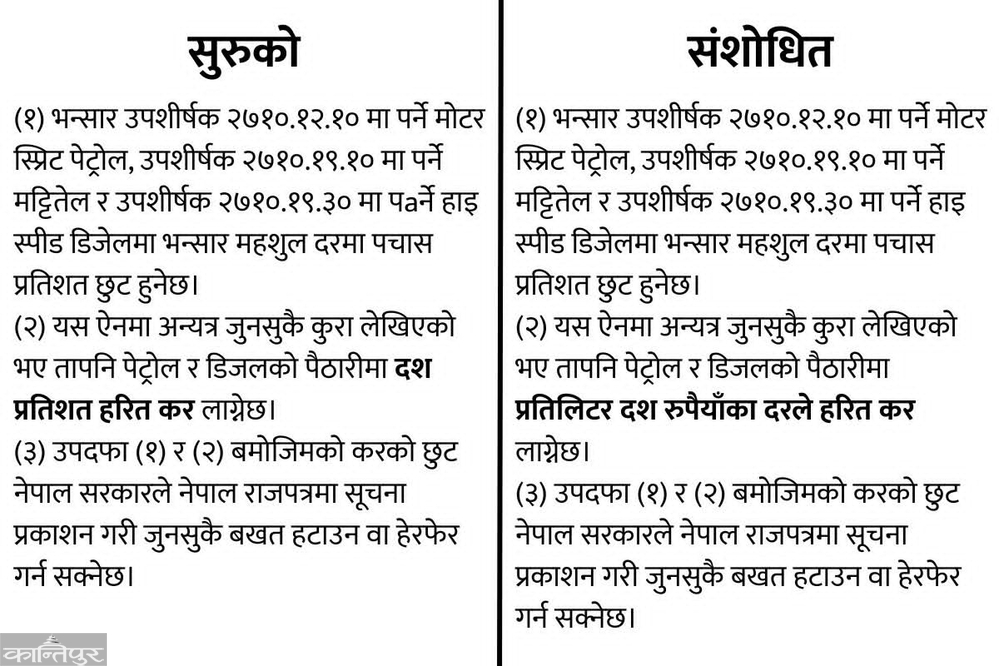

Third, the government has also amended the economic bill in the provisions related to customs duty on fuel and green tax exemption. In which initially the import of petrol and diesel was 10 percent per liter. By amending it, the government has said that ‘notwithstanding anything else written in this Act, a green tax of Rs 10 per liter shall be levied on the import of petrol and diesel.’ This provision seems to have been corrected by adding a percentage instead of a rupee.

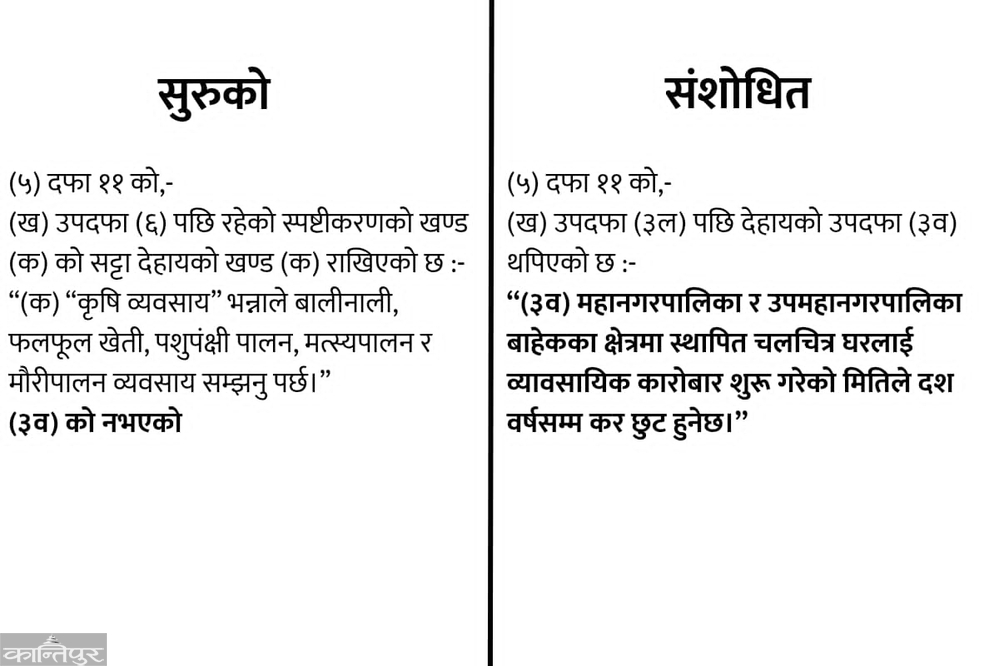

Fourth, the government has made a provision in the Finance Bill to provide tax exemption for ten years to cinema halls established in areas other than metropolitan cities and sub-metropolitan cities by adding 3 (b) to Section 11 of the Income Tax Act. Finance Minister Wagle had mentioned this in his budget speech. He had said that a provision has been made to provide complete income tax exemption for the first ten years to those establishing new cinema halls in areas other than metropolitan cities and sub-metropolitan cities. However, this issue was not included in the initial Finance Bill. In the latest bill, a provision has been added to Section 5 of Sub-section 11 of the Income Tax Act by adding 3(b) to Clause (b) to ‘Movie houses established in areas other than metropolitan cities and sub-metropolitan cities shall be exempt from tax for 10 years from the date of commencement of business.’

Fifth, Section 11 of the Income Tax Act has been added to Section 16(b) to provide that ‘Notwithstanding anything contained elsewhere in this section, if a natural person has insured a private building owned by him with a resident insurance company, the annual premium paid for such insurance or ten thousand rupees, whichever is less, shall be deducted from the taxable income and the tax shall be calculated as per this section only on the remaining amount. This provision was also in the budget statement. But it was not in the Finance Act. It has been included through an amendment.

Sixth, by amending the bill, the government has made a provision to allow a person to deduct 25 percent of the annual amount paid to a resident person for the education of his children as tuition fees or 25 thousand rupees, whichever is less, from the taxable income. ‘Notwithstanding anything contained elsewhere in Section 16 (b) of the Act, the tax shall be calculated on the remaining amount after deducting 25 percent or 25,000 rupees, whichever is less, of the annual amount paid by a resident natural person to a resident for the education of his children, from the taxable income,’ the latest bill states. This provision was not present in the original bill.

Finance Minister’s cleverness

After the repeated amendments to the economic bill, many questions have been raised in the media and social media linking Finance Minister Wagle. He has been defending his move by answering some questions at public events. After it was discovered that there were some ambiguities and some linguistic errors in the bill, the Ministry of Finance sent a request to correct the errors and the corrected matter to the Federal Parliament Secretariat on 17th Jestha, according to Minister Wagle’s secretariat.

Along with this, Finance Minister Wagle has registered a new economic bill in the House of Representatives on 17th Jestha. On page 465 of the bill, it is mentioned that an error has been corrected in the Economic Bill 2083 received from the Finance Minister's letter on 17 Jestha. When Kantipur inquired whether the Finance Minister can change one economic bill on 15 Jestha and revise tax rates and then present another bill on 17 Jestha, Ekram Giri, spokesperson for the House of Representatives Secretariat, said, "This is a government bill. The Finance Minister tabled the economic bill on 15 Jestha. Later, he corrected it and sent it. The government itself came with a letter stating that there was an error in the government bill, and the secretariat updated it."

However, he said that the discussion on the economic bill has not yet begun in the parliament. "The house is obstructed. Once the economic bill is registered in the parliament, its sections and subsections become active immediately," Giri added. Spokesperson Giri clarified that although the House of Representatives Rules 2083 contain provisions on the method, process and other provisions for registering bills in the parliament, there is no provision for revising tax rates.

What is the legal basis?

Along with presenting the budget in the federal parliament, the Finance Minister also presents the Appropriation Bill, the National Debt Collection Bill, and the Economic Bill. Along with the budget, all of these bills take the form of an act only after they are passed by the parliament. However, some provisions, including customs, come into effect the next day. However, there is a major difference in the issues mentioned in the Economic Bill presented by Finance Minister Wagle in the parliament on 15 Jestha and the Economic Bill last uploaded on the website of the Ministry of Finance. There is no legal basis for this. Because there is no law that allows the Finance Minister to amend the budget and bills after they are presented by the parliament.

Section 18 of the Economic Act provides that the Finance Minister can reduce, increase, or grant exemptions to tax rates. However, this provision is only for the period from 1 Shrawan to the next year's budget (15 Jestha). After the budget is implemented, the Finance Minister can revise the tax rates only after completing the process based on necessity and justification.

The process here means that along with the decision of the Ministry of Finance to revise the rates, the matter must be passed in the Council of Ministers meeting and the amendment must also be passed by the House. However, in some cases, Section 18 of the Act has given the Ministry of Finance and related ministries the right to increase or decrease tax rates. However, this provision is also for after the budget is implemented, i.e. before 1 Shrawan to 15 Jestha.

Did the Finance Minister make amendments without the law?

There is no legal provision anywhere regarding whether tax rates can be revised or not before the budget is passed by Parliament. Therefore, even now, there is no legal basis for the amendments made by Finance Minister Wagle. However, this is not the only year that the financial bill has been amended in this way. In previous years, minor errors were also amended in the bill. Finance Minister Wagle has told Kantipur that the bill has been amended 40 times before.

Since there is no legal provision like this, there is no basis for amending the bill. This has been done practically for a long time in the past. However, former finance ministers and former finance secretaries claim that even though the bill was amended with minor errors, the tax rates did not change as much as they do now.

What is the legal basis for amending the bill?

The House of Representatives Rules 2083 BS provide for the preparation, amendment and passage of bills. Chapter 17 of the rules contains the procedure for appropriation and finance bills. It includes the method and process for presenting, discussing and passing other bills in parliament along with the budget. However, this rule also does not have any legal basis for amending tax rates.

Finance Minister's clarification

Finance Minister Wagle has given a clarification regarding the amendment of the economic bill. In a clarification received through his secretariat, it is said that after it was discovered that there were some ambiguities and some linguistic errors in the economic bill presented in both houses of parliament on 15th Jestha, the Ministry of Finance sent a request to correct those errors and the corrected matter to the Federal Parliament Secretariat on 17th Jestha.

The clarification has reminded that Finance Minister Wagle's request for amendment of the bill and the issues where errors have been corrected and clarified are mentioned point by point 1 to 5. The statement states that since the economic bill is more sensitive than other bills and tax rates are implemented as soon as it is presented in Parliament, if the errors seen in it are not addressed immediately, there will be a big difference in the market and revenue.