Along with interest income, income (non-interest income) from remittances, digital transactions, letter of credit guarantees, treasury bills, service fees, etc. is also a factor.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

In the first nine months of the current fiscal year (from Shrawan to Chait), 20 commercial banks have earned a net profit of more than Rs 49 billion. The gross profit has increased by about 19 percent during this period compared to the third quarter of the previous fiscal year, according to the raw financial statements published by the banks.

Banks have said that net profit has increased by about 19 percent due to an increase in income (non-interest income) from remittances, digital transactions, letter of credit guarantees, treasury bills, service fees, etc. during this period. They say that the decrease in the amount of provisions that banks have to keep for non-performing loans and an increase in interest income during this period have had a positive impact on profit growth. In the third quarter of the previous fiscal year, 20 commercial banks earned a net profit of about Rs 41 billion.

Although the average profit of commercial banks has increased, the profit of 7 banks has decreased by last Chait. The financial statements mention that the profit of banks has decreased by a minimum of four to a maximum of 55 percent. However, bankers have said that overall, the profit of banks has increased in the third quarter.

Along with interest income, income (non-interest income) from remittances, digital transactions, letter of credit guarantees, treasury bills, service fees, etc. is also a reason. Lower interest rates have increased the borrower's payment capacity and this has had a positive impact on the bank's profit as it has reduced the bank's bad assets (NPA), says former banker and chartered accountant Analraj Bhattarai. 'Interest has come down a lot. For example, instead of paying interest of Rs 120 million earlier, now it is Rs 60 million. This has increased the borrower's payment capacity,' he said. 'The latest directive of the National Bank has prevented the bad loans of loans flowing to certain sectors, including productive ones, from increasing. Thus, the reduction in interest rates and policy easing have had a positive impact on the bank's profit growth,' Bhattarai said.

He said that the increase in the supply of money in the market during the 21 Falgun elections and the movement of business to some extent have also had a positive impact on the bank's balance sheet. ‘During the interim government, the Ministry of Finance released more than 9 billion rupees as interest subsidy,’ he said, ‘This has

On the one hand, the interest that banks could not collect has been recovered, and on the other hand, bad loans have decreased after paying interest.’

Bhattarai said that the fact that credit expansion by about 4.5 percent despite the failure to flow as per the target was also the reason for the decrease in bad loans. ‘In the past, many people used to flow new loans, due to which bad loans seemed to be low, but in the past few years, bad loans have increased because many people could not increase the flow of credit. Now, as loans are slowly increasing again, there are signs of improvement in bad loans.’

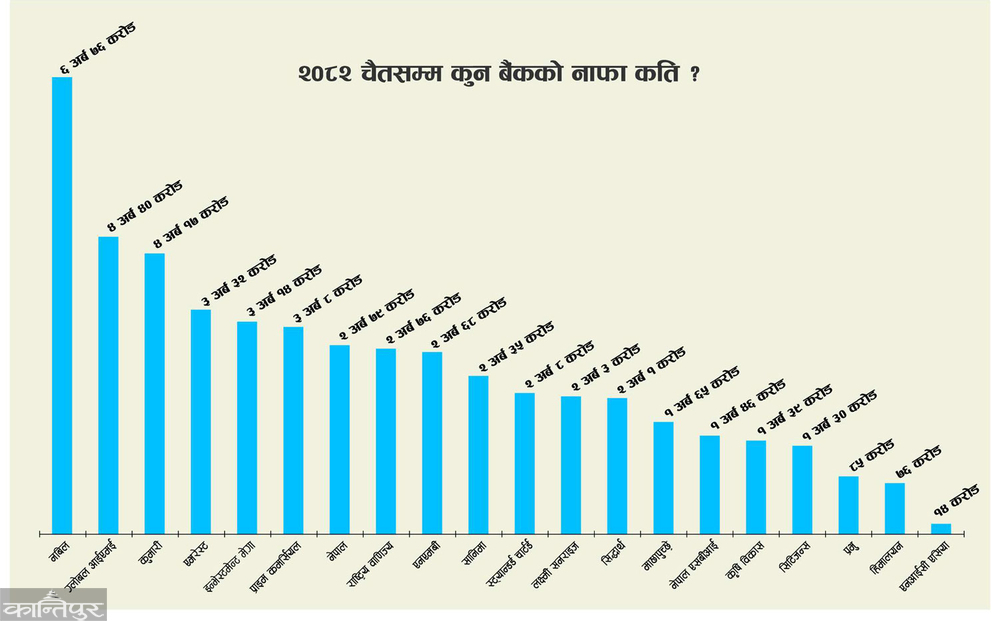

Among the banks whose profits decreased in the third quarter of last Chaitra (third quarter) are Prabhu, Nepal Investment Mega, Krishi Bikas, NIC Asia, Global IME, Everest and Standard Chartered Bank. Thus, Nabil Bank is at the forefront in terms of profit amount. Nabil Bank has earned a net profit of Rs 6.76 billion in the third quarter. Global IME Bank is second with a profit of Rs 4.40 billion, Kumari Bank is third with a profit of Rs 4.17 billion, Everest is fourth with a profit of Rs 3.32 billion and Nepal Investment Mega Bank is fifth with a profit of Rs 3.14 billion. Looking at the financial statements, the size of the balance sheets of the mentioned banks is also high, as the size of their profits is large. Of the five mentioned banks, except Nabil and Kumari, the profits of three have decreased in the same period this year compared to the third quarter of last year.

Although banks and financial institutions have not expanded their loans as expected in the last nine months, net profit has increased by about 19 percent due to increased loan recovery, decreased bad loans and increased non-interest income, said Santosh Koirala, President of the Nepal Bankers Association. Although banks and financial institutions have not expanded their loans as expected in the last nine months, net profit has increased by about 19 percent due to increased loan recovery, reduced bad loans and increased non-interest income, said Santosh Koirala, President of the Nepal Bankers Association. ‘Income other than interest income including remittances, digital transactions, letter of credit guarantees, treasury bills, service fees and others has increased in recent months,’ he said, ‘Mainly small loan recovery has increased. There has been a positive improvement in the tendency of customers to repay after taking a loan. He says that the financial condition of banks will improve further in Ashar. He says that since Ashar is the end of the fiscal year, there is a possibility of recovering a lot of loans, so the profitability of banks will improve.

The bad loans of banks have increased by 0.27 percentage points in the third quarter. In the third quarter of the last fiscal year, the average bad loans of banks were 4.98 percent, but it has increased to 5.25 percent in the same period this year. The bad loans of five banks are above 7 percent.

Generally, there is a provision to keep the bad loans of banks and financial institutions within 5 percent. Even if it goes beyond that limit, the Rastra Bank cannot take action against the bank. Because in such a situation, the action taken by the National Bank is not to give the fixed deposits it keeps to the banks. One of the qualifications that the National Bank must meet when it asks banks to bid for the amount in its various funds to be placed in fixed deposits is the bad debt limit. However, in recent years, the National Bank has increased this limit from 5 percent to 8 percent. This means that even if there is a bad debt of up to 8 percent, the National Bank will not be subject to action.

As of last Chaitra, banks have allocated 34.4 billion rupees in the provision for bad loans. In the same period last year, such limit was 34.81 billion rupees. It seems that the amount allocated by some banks for bad loans in previous years has been recovered this year. The net interest income of banks in the third quarter has increased by about two percent. Accordingly, the net interest income, which was 139 billion rupees in the third quarter of last year, has reached 142 billion rupees in the same period this year.

Accordingly, the net interest income of Rastriya Banijya Bank has increased the most by 23 percent. But the net interest income of half a dozen banks has declined. Despite the increase in profits, only about a dozen and a half banks are in a position to declare dividends.

The National Statistics Office has made an initial estimate of the growth rate of the financial and insurance sector in the current fiscal year at 9.16 percent. Accordingly, the office estimates that the financial and insurance sector will contribute 6.72 percent to the gross domestic product (GDP) in the fiscal year 2082/83.

The growth rate of this sector is expected to increase due to the increase in deposit and loan flows in banks, increase in renewal premium collection of non-life insurance and life insurance, and increase in the social security fund, provident fund, citizen investment fund, and securities trading, including commercial and merchant banks. The revised estimate is that the growth rate of the financial and insurance sector will be 7.55 percent in the fiscal year 2081/82.