As of March 11, banks and financial institutions had lent out Rs 1.22 trillion and 90 percent of deposits, but only 74.29 percent of the loans were disbursed.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

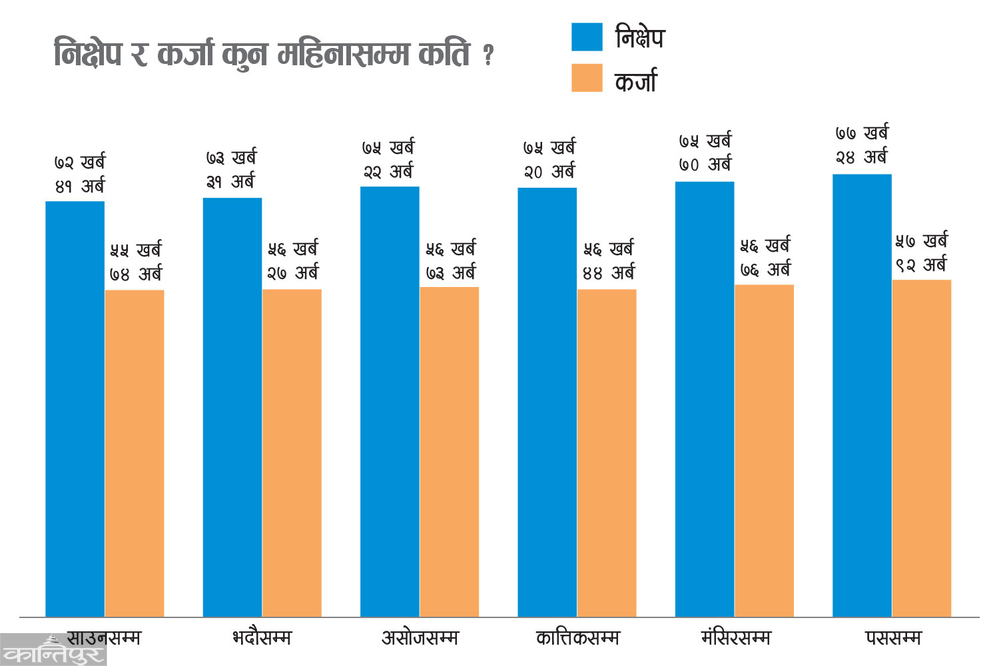

In the first seven months of the current fiscal year (Shrawan to Magh), banks and financial institutions have collected deposits worth Rs 431 billion, but have disbursed loans of only about half of that amount, Rs 214 billion. This data is as of last Monday (11 Falgun).

Although the deposit collection of banks and financial institutions has increased this year compared to the same period of the last fiscal year, the credit flow seems to have decreased. Accordingly, banks and financial institutions had collected deposits of Rs 256 billion and disbursed loans of Rs 272 billion by the end of the last fiscal year.

While the investment environment in the country has not improved, the unstable situation created after the Gen-G movement of 23 Bhadra and the protests of 24 has worsened the situation. This is confirmed by the fact that deposits have increased during the same period of this year compared to the seven months of the last fiscal year, but the credit flow has decreased.

With the expansionary budget and monetary policy in the current year, it was expected that the credit flow would increase and the loanable amount accumulated in banks would decrease. There were signs of an increase in loan demand in the initial months. However, the data on credit flow for about seven and a half months does not have any possibility of meeting the objectives of the National Bank. Due to the lack of credit flow, more than 100 billion loanable amount (excess liquidity) has been continuously accumulated in banks and financial institutions.

Interest rates have fallen to their lowest point in history. According to the general theory of economics, there is an inverse relationship between interest rates and credit flow. When interest rates fall, credit increases, and when they rise, it decreases. This principle does not seem to be working at present. Experts say that even though interest rates have fallen, other factors are still active, so the demand for credit has not increased.

Nepali industrialists say that industrialists have not been able to invest more due to political instability and security concerns. Despite the desire to increase investment, they claim that the country's investment environment and security situation are critical.

Nepal Chamber of Commerce President Kamlesh Agrawal said that the demand for credit in banks has not increased as more than 1.5 lakh borrowers have been blacklisted in the last five years and the private sector has not been able to build capital. 'Meanwhile, banks and financial institutions have started selling collateral in a hurry to recover loans. This led to a decrease in the valuation of securities, which in turn reduced the morale of the private sector, he said. "The investment environment did not improve due to political instability in the country and the inability to guarantee security in the personal and business sectors."

However, bankers say that there are signs that loan demand has gradually increased in the last few weeks. Especially after the Rastra Bank adopted policy flexibility in various sectors, loan demand has started increasing in real estate, shares, personal overdrafts, etc., says Devendra Raman Khanal, Chief Executive Officer of Rastriya Banijya Bank. "As a result, loan demand from the real sector including industry, trade, large infrastructure has not been able to increase," he said. "Although it has been slow in recent months, there are ample signs of loan demand increasing." Khanal said that since the election is scheduled to be held next week, the demand for loans may increase as political stability will prevail after the formation of a new government.

The Rastra Bank has set a target of 12 percent loan expansion for the current fiscal year. For this, an additional loan of about Rs 5.5 trillion needs to be expanded. Experts say that the annual target is unlikely to be met, given the situation for the past seven months.

Financial sector expert Parashuram Kunwar Chhetri said that the recent developments in the country have not created an investment environment. He said that work should be done to increase the confidence of the private sector as the confidence has dropped significantly.

However, with sufficient liquidity in the market, there is ample opportunity for investment for the new government to come. ‘There is no situation where there is no money for development. There is liquidity in both domestic currency and foreign currency. There is no situation where there is no dollar when the government imports capital equipment including information technology, machinery, if it wants,’ he said. ‘The government can borrow money from the market at a cheap interest rate and invest in large infrastructure and national pride projects.’

By the end of the seven months of the current fiscal year, banks and financial institutions have accumulated a loanable amount (excess liquidity) of Rs. 1.22 trillion. Liquidity has been accumulating in banks for about three years. The increase in remittances in recent days has accelerated the accumulation of money in banks. As of 11 Falgun, the total deposits in banks and financial institutions are 7735 billion. The credit-deposit ratio (CD ratio) during the same period is 74.29 percent.

As per the instructions of the National Bank, banks and financial institutions are allowed to lend up to a maximum of 90 percent of the total deposits. The total credit flow of banks and financial institutions during this period is 5850 billion. Based on the above data, banks and financial institutions have an amount of 1227 billion rupees that can be lent (excess liquidity) as of mid-Asard. However, banks and financial institutions must keep 20 percent of their total deposits in cash in the bank.

Thus, the amount that all banks and financial institutions must keep with them to maintain 20 percent liquidity is about 1 percent of the CD ratio. Based on this, although banks are allowed to lend up to 90 percent of deposits, in practice they are allowed to lend only up to 89 percent. Based on this, the amount of 1149 billion rupees that can be lent to banks and financial institutions has accumulated.

After the liquidity in the banks piled up, the National Bank has announced to revise the scope and limit of sectoral loans. Through the semi-annual review of the monetary policy for the current fiscal year released on Tuesday, the National Bank has announced that it is going to expand the scope of sectoral loans and also revise the existing rate related to the minimum loan ratio to be maintained by banks and financial institutions in those sectors. In which, the National Bank is preparing to include tourism, information technology and export-oriented industries based on domestic raw materials in the scope of the sectoral loan limit implemented with the aim of encouraging credit expansion in agriculture, energy and micro, household and small enterprises/businesses.

Through the review, it is trying to facilitate credit flow, encourage credit flow in the information technology and AI sectors. The National Bank claims that it is trying to increase overall economic activity by further encouraging banks in areas with investment potential, expanding investment in areas where production and employment are created, diversifying investment and facilitating the process of repaying loans to borrowers. For this, the NRB has announced in its monetary policy that it will provide more flexibility in working capital loans and facilities such as loan rescheduling and restructuring to borrowers who are in difficulty due to circumstances.