Due to the circumstances, there has been a slowdown in business and the number of blacklisted debtors has increased due to non-payment of loan principal and interest, the task force has suggested to be flexible in the related instructions for some time.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

The Banking Sector Reform Suggestion Task Force formed under the coordination of Revat Bahadur Karki has submitted its report. The working group submitted its interim report last Tuesday and submitted its final report to Governor Vishwanath Paudel on Monday.

According to the

report, the banking policy rules should be made liberal and prudent, the current guidelines on directed loans should be amended, banks and financial institutions should be classified on the basis of capital, performance, etc. There are suggestions in the report, including the need to adopt a risk-based supervision system, and to loosen the existing system related to bad loans.

Sources have said that the task force has suggested extensive changes in the current policy rules and guidelines of the banking sector to make the slogan 'healthy regulation, healthy banks and customer-friendly banking' meaningful. The report also suggests that risk-based supervision should be made effective and banks should be classified based on level (performance).

The task force has also suggested to revise the current loan classification and bad loan loss management system and revise the policy according to the quality of loans and good international practices. In next year's budget and monetary policy, the issue of establishing an asset management company has been covered for the management of increasing bad loans. However, the task force said that bad debt management cannot be managed only by establishing a company, and looking at international successful practices in terms of debt classification and loss management, the task force has asked to formulate a policy accordingly. "A special powerful task force should be formed for bad debt management, in which there should be representatives of private sector banks and financial institutions," the source said, "The task force should study in detail and look at international successful practices and make a policy arrangement accordingly."

There is a provision that about 45 percent of the total loans disbursed by banks and financial institutions should be invested in the priority and underprivileged sectors designated by the National Bank. The bankers complain that this system is very old, in the financial year 2063/64, directed loans other than the needy were suspended but started again, because of this directive, they are not able to do business freely. The working group has suggested to amend the existing arrangement in this regard.

The current regulatory system is very strict and since the National Bank is doing micro-regulation, the working group has said that it should be reduced to make the supervision system more effective. The conclusion of the task force is that due to the strict instructions of the National Bank and the lack of demand creation in the economy, loans have not been disbursed as expected. For this, the working group suggests that policy guidance should be flexible for some time and the working capital loan guidelines should also be revised.

Based on the conclusion that business has slowed down due to circumstances and the number of blacklisted debtors has increased due to non-payment of loan principal and interest, the task force has also suggested to be flexible in the related instructions for some time. "Since the economy is in a slow state, they will ask the government for tax exemptions and the National Bank can also create an environment for credit expansion by giving various exemptions," the source said.

Banks and financial institutions have stopped disbursing interest subsidized cheap loans for the past two years because the government did not provide the amount for the interest subsidy. Banks are charging full interest even to borrowers who have taken subsidized loans in the past. In such a situation, until the money comes from the government, the working group has also asked the Rashtra Bank to continue the subsidized interest rate loan program by managing the amount for the interest subsidy itself.

Nepal Rastra Bank formed a three-member working group a month ago under the coordination of Karki to submit suggestions for the overall improvement and strengthening of the banking sector. Bhuwan Kumar Dahal and Executive Director of Bank and Financial Institutions Regulation Department of Nepal Rastra Bank Guru Prasad Paudel were members of the working group.

The time of the task force is one month and the report has been submitted within the specified time. In the report, banking policy regulation should be liberal but prudent (prudential), risk-based effective supervision and development of customer-friendly banking services, banking sector should play to make economic activities fully operational. The

task force was given a mandate to take measures to make credit flow effective in rural areas, merger and acquisition of banks and financial institutions and identification and solution of the problems after that action, the banking sector should play to remove Nepal from the gray list, and the coordination mandate of the Central Bank in the development of the capital market.

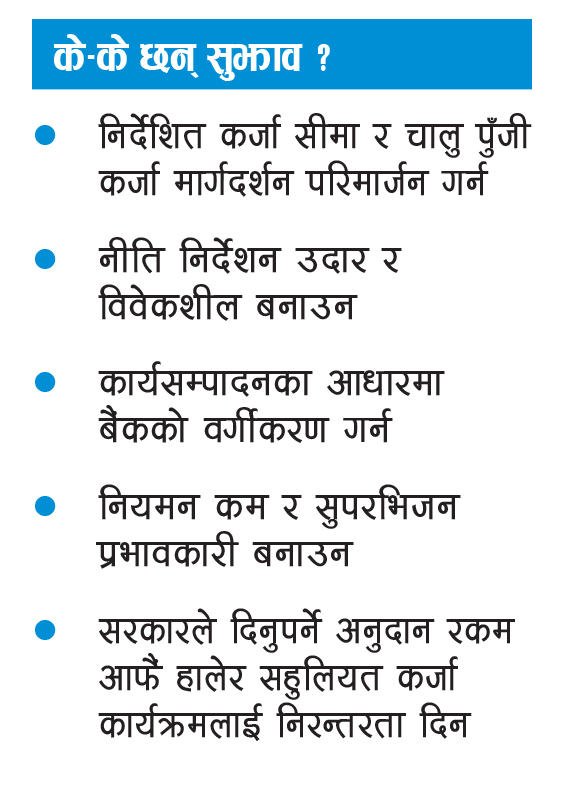

What are the suggestions?

– To revise the guideline credit limits and working capital credit guidelines

– To make policy guidance liberal and prudent

– To categorize banks based on performance

– To make regulation less and supervision effective

- To continue the subsidized loan program by adding the subsidy amount to be given by the government.