The budget for the fiscal year 2083/84, which the government presented to the federal parliament on Friday, and the subsequent financial bills have created some confusion among many taxpayers.

We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

The budget for the fiscal year 2083/84 presented by the government in the federal parliament on Friday and the subsequent economic bills have created some dilemmas among many taxpayers. Among those questions, an attempt has been made to discuss the provisions of the income tax, value added tax and economic bills made in the budget here.

Section 57 of the Income Tax Act not applicable

In Section 57 of the Income Tax Act, the Economic Bill 2083 has made a provision that Section 57 will not be applicable in the following cases: First, in startup venture capital and private equity funds, the capital of the existing shareholders and partners remains unchanged and new shareholders and partners are added, and the capital is increased. Second, in the event of the death of the beneficiary of the entity, the interest in the entity is involuntarily relinquished and transferred to the legal heir. Third, in the event of a change in the ownership of a resident entity, which is the reason for the change in the ownership of another resident entity in which the entity has an interest.

The latter two cases apply only to changes in ownership that occur after 1st Shrawan. In other cases, if the share ownership in a company or partnership changes by 50 percent or more, Section 57 applies. In startup venture capital and private equity funds, Section 57 does not apply only if the capital of the existing shareholders and partners remains the same and new shareholders or partners add new capital. This provision does not apply to other entities.

Similarly, a provision has been added that Section 57 does not apply if the share structure changes due to the involuntary termination of the interest due to the death of the beneficiary. Since this provision has also been decided in the Supreme Court's sentencing order 080-WO-1506 dated 11 Bhadra 2081, it seems that an attempt has been made to include this situation in the Income Tax Act.

This bill has added only a third situation to the provision of Section 57. In the case of a Nepali resident company investing in another company, the ownership of the investing company changes and the situation of another resident entity in which the company has invested has also been removed. For example, if a Himalayan company registered in Nepal transfers its rights among its shareholders and changes its ownership, Section 57 will be applicable to a Pahad company registered in Nepal, in which 90 percent of the shares of the Himalayan company are invested, whereas Section 57 will not be applicable to a Pahad company after the amendment. As a result, even if Section 57 is applicable to a Himalayan company, Section 57 will not be applicable to a Pahad company.

The business world has considered Section 57 or Section 95A of the Income Tax Act as one of the most complex provisions of the Income Tax Act. Many expected the new government to make fundamental changes to one of these two sections, but there has been no amendment accordingly. However, the aforementioned amendment has helped reduce administrative complexity to some extent.

Capital gains tax to be final for natural persons and entities

Capital gains tax to be final for natural persons and entities

Capital gains tax is applicable only to natural persons as per the Income Tax Act 2058. Profits from the sale of land, buildings and share investments in entities (companies, partnerships, etc.) are taxed at the normal rate. Although there was a provision earlier that natural persons were required to submit income statements on profits received from share investment, land and building sales, but there was a provision that no additional tax would be levied, a provision has been added that the advance income tax paid on profits received by resident natural persons or non-resident persons who do not want to submit income statements will be final. This provision has resolved the doubts among investors.

Amount received from abroad will be final

Income received from banks, financial institutions or remittance companies for providing software or other electronic services from outside Nepal after deducting 5 percent tax, income received from consulting services abroad by any resident natural person who is not involved in business operations, income received from the use of social media, and one percent advance tax deducted by resident e-commerce platforms will be final tax deducted. Thus, no additional tax will have to be paid on the amount with final tax deduction. Earlier, in the case of taxpayers with such income, it was necessary to submit an income statement even though no additional tax was levied as per Sub-section 4A of Section 1 of Schedule 1 of the Income Tax Act.

It has solved the administrative liability of taxpayers who earn income using social media, riders who drive bikes and cars, and natural persons who provide IT services. However, taxpayers who earn an annual income of Rs 4 million or more, who also have other income in addition to such taxes, are required to submit the De-04 statement annually.

Tax on income from employment

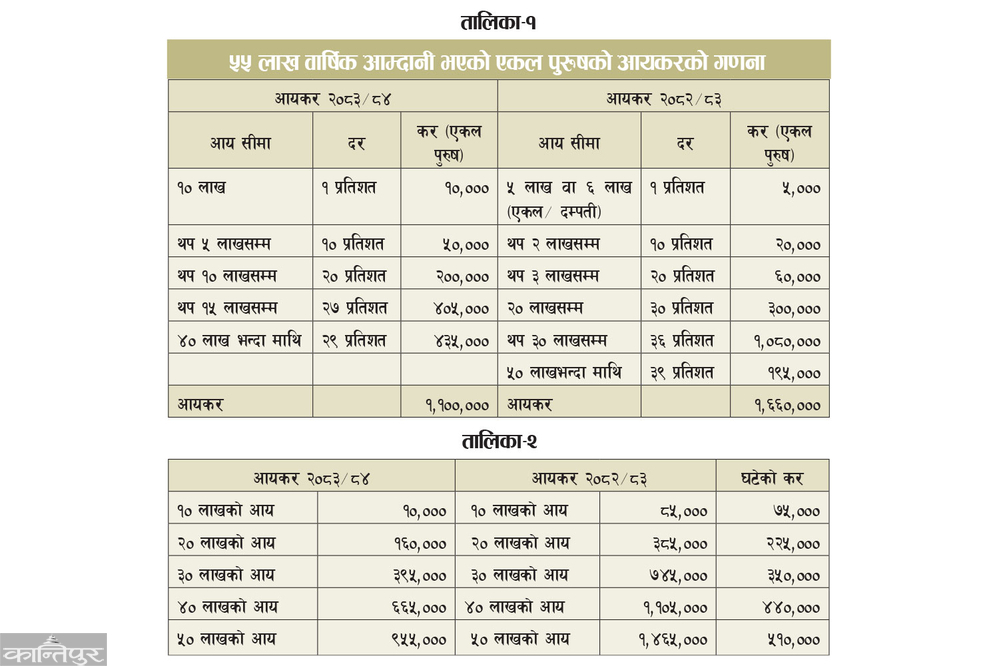

Taxpayers have taken the income tax provision made on employment income through the Finance Bill 2083 as a great relief. The tax rate has been kept the same for both single and couple cases. Earlier, there was a provision that up to Rs 5 lakh was not taxed in the case of a single person and Rs 6 lakh in the case of a couple or only one percent was levied. Table-1 presents the income tax rates and limits for 2082/83 and 2083/84 comparatively.

According to the said rate, the tax liability of a single male taxpayer in 2082/83 and 2083/84 will decrease in the various income limits as per Table-2. In the case of female taxpayers, the tax liability is reduced by 10 percent.

The amount that can be deducted in calculating tax for home insurance has also been increased from 5,000 to 10,000. This also seems to reduce some tax liability.

Reducing tax rates and increasing tax base

Reducing tax rates and increasing tax base, although the theoretical issue of increasing tax base is easy to hear and say, is just as complicated in tax policy formulation. The pressure on resources when reducing tax rates and the lack of scope to increase the base are the most complex issues in budget formulation.

It seems that efforts have been made to manage the resources required when reducing the employer's income tax rate to some extent by making use of passive income known as profit from the sale of real estate and the sale of shares of listed companies. The tax rate on active income such as employment has been reduced, and the tax rate on income from the purchase and sale of real estate and investment in shares of listed companies has been increased slightly.

The tax rate on profit from real estate sold within five years has been increased from 7.5 percent to 10 percent. The tax rate on gains from the sale of real estate sold after a period of more than five years has been increased from 5 percent to 7.5 percent. Similarly, the tax rate on gains from the sale of shares of listed companies sold within a period of less than 365 days has been increased from 7.5 percent to 10 percent. The tax rate on gains from the sale of shares of listed companies sold after more than 365 days has been increased from 5 percent to 7.5 percent. Although tax collection on gains from the purchase and sale of shares of listed companies is simple, there is a need for a scientific method to determine the value of real estate to strengthen the collection of tax on the purchase and sale of real estate.

With the aim of expanding the scope of the tax, the old health service tax and education service tax have been renamed as health equity fee and education equity fee as new equity taxes. Private sector health service providers and educational institutions must collect and pay 3 percent equity tax on all types of fees from service recipients. This seems to make private education services and private health services more expensive by 3 percent.

Addressing the demands of entrepreneurs

This bill seems to address most of the demands made by entrepreneurs during the tax policy discussions. The demand for implementing multiple rates on VAT has been made by entrepreneurs since 2052 BS, but every government has not implemented multiple rates citing administrative complexity.

When a person operating a ride-sharing service (ride-sharing operator) connects to a platform operated by a person providing transportation and transportation services, a five percent value-added tax has been imposed on the person operating the ride-sharing service and the person providing electricity services to the end consumer (Nepal Electricity Authority), thereby imposing multiple rates on the value-added tax.

With this, the Nepal Electricity Authority and Butwal Power Company will collect 5 percent value-added tax from customers. This has increased the value-added tax rate from 3 to 4 rates. Under this, there are situations where there is no value-added tax, tax at a zero rate, value-added tax at a rate of five percent, and value-added tax at a rate of 13 percent.

While efforts are being made to bring GST from multi-rate to single-rate in India, in Nepal, the justification for other taxes such as TSC, green tax will not be theoretically justified when multiple rates are applied to the value-added tax. Multi-rate value-added tax, excise duty, customs duty and taxes such as green tax, luxury tax, film development fee, parity fee, telephone service fee, etc. specified annually by the Economic Act, seem to complicate tax administration. If other taxes are kept as they are in addition to the multi-rate value-added tax, the reason and logic for implementing the value-added tax will not be valid.

In addressing other demands, it seems that an attempt has been made to address the demands of businessmen by reducing the tax assessment period by the Internal Revenue Department from four years to three years. The deadline for claiming income tax refund has been increased from two years to five years. However, in practice, even before, even after tax assessment within four years, businessmen's tax has been assessed by mentioning issues such as tax evasion. There is no example of any action being taken against employees involved in tax assessment in this way.

The time limit for claiming tax refunds has been increased from two years to five years, while the system for automatic income tax refunds should be implemented. If there is an adjustment between the liability and various taxes to be collected in case of overpayment of value added tax, income tax and other taxes prescribed by the Economic Act, it would seem that there would be more ease in tax administration.

A provision has been added to allow deduction of expenses incurred in professional social responsibility subject to 1 percent of taxable income. The limit of expenses for donations has been increased from one lakh to three lakh. Similarly, a provision has been made to allow expenses incurred while issuing shares and debentures to be claimed as expenses. These provisions seem to have been added to clarify the tax assessment orders made by the tax office after the tax assessment of various taxpayers, rather than allowing or not allowing expense claims based on the principle of income tax.

The tax rate on the commission income of insurance agents has been increased from 15 percent to 20 percent. Similarly, insurance agent services have been included in the list of non-VAT and relief has been provided to insurance agents and life insurance companies by providing exemptions from income tax, VAT, interest, fees, penalties and details applicable to their previous income.

This arrangement has brought ease in tax compliance. However, despite the fact that tax is assessed every year for the life insurance business, the Income Tax Act implemented since 2058 BS and the Value Added Act implemented since 2052 BS have not been complied with even up to 2083 BS, as is evident from the dilemma faced by insurance agents in income tax and value added tax.