We use Google Cloud Translation Services. Google requires we provide the following disclaimer relating to use of this service:

This service may contain translations powered by Google. Google disclaims all warranties related to the translations, expressed or implied, including any warranties of accuracy, reliability, and any implied warranties of merchantability, fitness for a particular purpose, and noninfringement.

53 trillion 48 billion rupees have been disbursed from banks and financial institutions. What percentage of this loan has been productive (in areas that contribute to economic growth)?

The answer to this question is not so easy. However, more than half of the total loans provided by banks and financial institutions seem to be invested in non-productive (not directly contributing to economic growth) sectors. The data mentioned is as of last Saturday .

The total loan disbursed by banks and financial institutions till last November is 52 trillion 85 billion rupees. On the basis of this data, sector analysis of loans has been done.

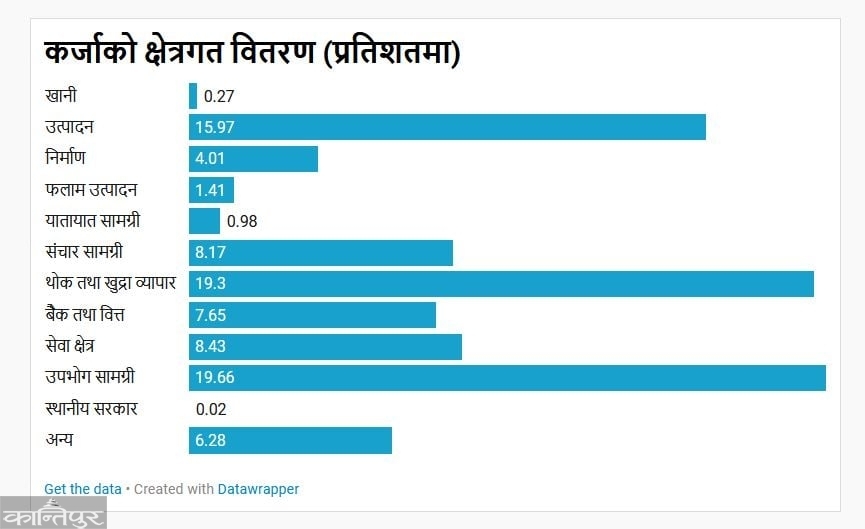

According to the sectoral classification of loans provided by banks and financial institutions, about 30 percent of loans are in the productive sector (agriculture and animal husbandry, manufacturing, metal and machine production, small and medium entrepreneurs, etc.) of Nepal Rastra Bank. The data is . Out of the remaining 70 percent, about 19 and a half percent went to consumption and 19 percent to trade (wholesale and retail), 8/8 percent to transportation and communication and service sector, and 4 percent to credit construction sector.

Similarly, according to the plan (product/scheme) brought by the banks and financial institutions for lending, it seems that about 52 percent of the loans are only for projects and long-term infrastructure (temporary loans) and working capital loans . Apart from this, about 12 percent of 'cash credit', 7 and a half percent of housing loans and 5 percent of real estate sector have flowed . Similarly, 5 and a half percent of credit has been given to the poor, overdraft, share and hire purchase of two percent. The data of Rashtra Bank has 8 and a half percent loan investment in others. When looking at the collateral taken by the bank while disbursing

loans, more than 78 percent are fixed assets. Of that, 66 percent is in real estate only.

Similarly, about 90 percent of the total loans provided by banks and financial institutions have been provided as collateral. Out of which, about 76 percent of fixed assets (including real estate) are mortgages and 66 percent of them are mortgages of houses and land, according to the data of Rashtra Bank.

However, very little credit has gone to project financing. Nar Bahadur Thapa, an economist and former executive director of Nepal Rashtra Bank, said that this confirms that even when giving loans for any purpose, banks are looking for fixed assets as collateral.

"If you don't have a house and land, you can't get a loan from the bank, so citizens have to invest in immovable property in order to qualify for a loan," he says. In order to increase the capacity, it has become necessary to invest in real estate. Due to the

policy arrangement, borrowers have increased investment in real estate in a roundabout way. Thapa argues that the banking sector cannot be linked to the real economy without major structural changes in the lending system.

Likewise, the government sets the target of economic growth and price increase in the annual budget announced on June 15 every year. The National Bank formulates monetary policy to help achieve the target set by the government. Looking at the relationship between budget (financial policy) and monetary policy, credit expansion from banks and financial institutions should directly contribute to economic growth. But the reality is completely different.

Although banks and financial institutions sometimes extend loans at high rates, the government data shows that they have made a negligible contribution to the country's economic growth.

Although banks and financial institutions occasionally extend loans at high rates, the government data shows that they have made a negligible contribution to the economic growth of the country . It is confirmed by the data that credit expansion is on one side and economic growth is on the other side. However, economists say that high credit expansion has contributed very little to economic growth as it has directly contributed to the increase in import prices, real estate, stock market, vehicles and other assets.

Economist Vishwas Gauchan argues that the loans provided by banks and financial institutions are contributing insignificantly to the economic growth of the country. Based on the data of the three decades after the liberalization of the 90s, a 1 percent increase in credit to the private sector has increased the economic growth rate by 0.23 percent, the inflation rate by 0.37 percent and the import growth rate by 0.75 percent. It shows," he says, "If the loans provided by the banks stayed within the economy, there would be no problem. There has been a problem in exiting that country through imports. He said that although credit expansion has increased economic activity, it has contributed little to production growth.

Banking sector larger than GDP

Total deposits in the financial system as of last October are about 16 percent higher than the size of the economy (Gross Domestic Product-GDP). Experts have analyzed this as the growth rate of the financial sector is higher than the economic activity of the country. They pointed out that although the growth of the financial sector is good, it is higher than the growth rate of the economy, so there is a possibility of risk. In such a situation, experts suggest that the policy maker should formulate the policy in a moderate manner.

As of the end of last October, the ratio of credit to GDP is about 93 percent. At some point in the past, the ratio of credit to GDP was 95 percent. After the reduction in credit expansion in recent years, this ratio has decreased.

A former executive director of the Rashtra Bank said that the growth rate of the financial sector is higher than the growth of the overall economy as the ratio of deposits to GDP exceeds 100 percent. In such a situation, any risk in the financial sector will have a big impact on the economy, according to his analysis. "It is good that the growth rate of the financial sector is high," he said, "Accordingly, the economy could not grow." Therefore, the possibility of risk is also the same.

In such a situation, capital cannot be created from the funds in the financial system. Therefore, he suggested to the National Bank that the policy makers should keep an eye on these things while making the policy.

The major contribution of credit has been to increase in imports, increase in the price of fixed assets including real estate, and after not contributing to economic growth as expected, the National Bank increased the share of credit directed by banks and financial institutions. About 45 percent of the loan has been disbursed.

30 percent credit in agriculture, energy and SMEs

According to the directives of the National Bank, by 2084, banks should transfer about 40 percent of the total credit to agriculture, energy and micro, domestic and small enterprises/businesses. Until last June, 13.2 percent of the total loans invested by commercial banks were in the agricultural sector i.e. 5 trillion 82 billion 49 crores, 7.9 percent i.e. 3 trillion 50 billion 74 crores in the energy sector and micro, domestic, small and medium 9.2 percent in the enterprise sector, i.e. 4 trillion 7 billion 28 billion, is the data of Rashtra Bank.

In the same period, 26 percent of the total loans in agriculture, micro, domestic and small enterprises/businesses, energy and tourism sectors from development banks i.e. 1 trillion 25.83 billion and 21.6 percent i.e. 19.38 billion loans from finance companies is in investment .

"Out of the total loan disbursements from commercial banks, an average of 5.79 percent i.e. 2.63 billion 70 million loans have been disbursed to the poor," said the National Bank, "from development banks." 8.16 percent i.e. 40.31 billion rupees and 6.70 percent i.e. 6.58 billion rupees loans from finance companies have flowed to the underprivileged.' Department Head Gunakar Bhatt said. "Energy, wholesale and retail trade and expansion in personal consumption loans and the recent situation of commodity imports seem to have started to increase economic activity," he said. However, credit is not being extended in construction, agriculture and other sectors. He said that if sectors such as construction and industrial production, which have been continuously shrinking in the past two financial years, expand, credit flow will also increase.

Credit expansion boosted property prices

Especially in Nepal, based on the data of the three decades after the liberalization of 1990, a 1 percent increase in credit to the private sector leads to 0.23 percent economic growth, 0.37 percent inflation and 0.75 percent imports. Various studies have shown that increasing the growth rate. During that period, the average annual private sector credit growth rate is 20%, economic growth rate is 4.4%, inflation rate is 7.5% and import growth rate is 15.7%.

Member of National Planning Commission and Executive Director of Rashtra Bank Prakash Kumar Shrestha also admits that credit expansion has not made the expected contribution to economic growth. Statistics also show this. But he says that such a situation has been created not because of the National Bank, banks or any other agency, but because of the priorities of the state, the National Bank, etc., which change at different times.

'In the past, credit expansion was high, economic growth rate was low . Credit has not increased in recent years, but the economic growth rate is satisfactory. The contribution of credit expansion is not to speed up the economic growth,' he said. However, the question has arisen as to how much the loan that has flowed in the directed sector has been invested in the right place.'

President of Nepal Bankers Association Santosh Koirala is not ready to accept that credit expansion has not contributed to economic growth. It is true that in the past, credit has decreased in areas where economic activity was active. Therefore, the contribution to economic growth may have been less,' he says, 'now the situation has changed . Rastra Bank has already issued guidelines including current credit guidelines. In recent years, all the loans have been transferred to the real sector . This is why credit expansion has contributed greatly to economic growth.

Now the size of the informal economy is 40 percent, the high officials of the National Bank have been saying publicly. Based on this data, the total economic activity (size of the economy) of Nepal is more than 57 trillion 5 billion rupees, i.e. at least 40 percent more.

On the one hand, informal transactions have not been included in GDP, on the other hand, the base of GDP calculation is wrong. When the foundation is wrong, the results are also wrong," said a former banker. That didn't happen, we moved towards credit contraction.

How much priority was given to the industry when the monetary policy was being introduced since 2002? A direct lending policy was introduced, microfinance licenses were distributed to encourage the rural economy. Now that's the problem. Asked to give hydropower loans without regional assessment, there was a problem. The official said that now there is a problem because they have not been able to make a long-term policy by doing things here and there.

credit expansion and economic growth

Looking at the data of economic growth, credit expansion and deposit collection in the last 11 years, credit expansion is faster than deposit collection in most years. According to which, in the financial year 070/71, when the credit increased by 19.12 percent, the economic growth rate was 6.01 percent .

In the financial year 072/73, the economic growth rate remained at 0.43 percent while credit expanded by 27 percent. Similarly, in the financial year 076/77, the economic growth rate was negative by 2.37 percent while credit expanded by 16.21 percent. Similarly, in the financial year 080/81, the economic growth rate is 3.87 percent while the credit expanded by 5.8 percent. In the last decade, the highest credit expansion was in the financial year 077/78 by 28.18 percent, while the lowest credit expansion was in the financial year 079/80 by 3.43 percent. In the last 10 years, the highest economic growth rate was 8.98 percent in the financial year 073/74 and the lowest was negative 2.37 percent in the financial year 2076/77.